While we love to talk about life, happiness and self-actualization a lot more than most financial planning firms, we’re still big nerds about financial planning. And today, we’re here to nerd-out just a little bit…and hopefully help a few people in the process!

Backdoor and Mega Backdoor Roth “Loophole” May be Closing

There’s been speculation that if Congress passes the Build Back Better plan during 2022, they might close the “backdoor Roth” loophole mid-year. We want to encourage everyone – and we’ll be in touch with our clients in the next couple of weeks – to go ahead and “front-load” their backdoor (and mega backdoor) Roth contributions for 2022. Meaning, go ahead and make those Roth contributions now, in January, or as early as you can. While elimination of the backdoor funding loophole midyear is probably unlikely due to the administrative mess it would cause, we still think it’s a good idea to get your contributions out of the way, early.

What’s so great about Roth accounts anyway?

Here are just some of the highlights:

- Tax free-growth, and tax-free distributions of growth post-age 59.5

- No required minimum distributions once you turn 72, unlike traditional IRAs/401(k)s

- Because of the prior two bullet points, Roth accounts are some of the best assets we can pass to the next generation – the money stays intact for longer, to grow tax free

- There are other flexibilities with Roths that make them an interesting parking spot for education savings – too deep to go into here, more on this in a follow-up blog post!

Backdoor? Loophole? Sounds a little complicated…

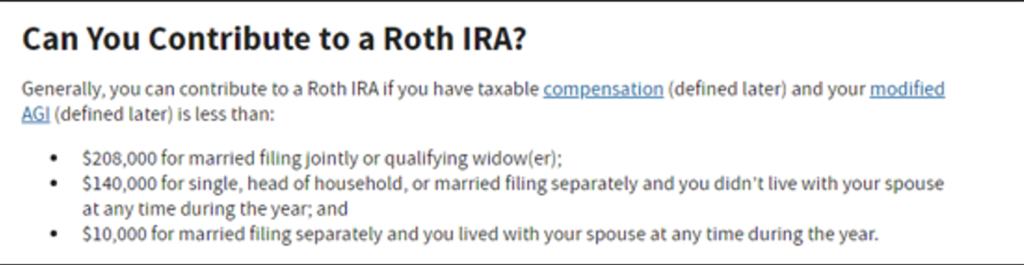

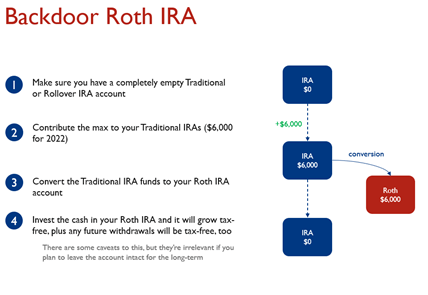

So what actually *is* a backdoor Roth? Well, it’s not a thing – it’s a series of steps that allows high-earning households to still be able to contribute to Roth accounts, despite being over the stated IRS income thresholds.

In other words, you might make too much money to make a Roth contribution. But… via the “backdoor” you can still save money into your Roth account.

This is a known loophole that’s been around for many years. Rather than being risky or on the edge, it is essentially sanctioned by the IRS and isn’t considered remotely risky or aggressive under current tax law.

What exactly is a “Mega” backdoor Roth contribution?

Now… here’s where it gets really interesting! Some of us actually have TWO opportunities to make backdoor Roth contributions. Up until now, the implied focus of this article has been on Roth IRAs. Certain 401(k) plans also allow for their own flavor of Roth contribution, dubbed a “mega backdoor Roth.”

With a mega backdoor Roth 401(k) contribution, you are actually making after-tax 401(k) contributions, then converting those dollars to a Roth, either inside your 401(k) or they can be rolled to an outside Roth IRA. Note: after-tax contributions are distinctly different from Roth 401(k) contributions. Make sure you’re clear that you’re making after-tax contributions, then converting, versus making Roth 401k contributions directly (which lowers amount you can put into your pre-tax contributions and lowers your overall tax savings!)

The reason that point is so important to make: you are only allowed to defer $20,500 of income into your 401(k) every year. That can be done either as a pre-tax contribution or Roth contribution. After-tax contributions DO NOT count towards the $20,500 maximum, and since they can be subsequently converted to Roth dollars, you have the opportunity to kill two birds with one stone (or “feed two birds with one scone,” as my husband likes to say): you can defer $20,500 pre-tax in order to lower your taxes, AND save even more into a Roth by way of the mega backdoor Roth contributions.

Here’s an article that we love, which goes into a lot more depth. But, to make a long story short, if your 401(k) plan offers the ability to make after-tax 401(k) contributions, please reach out! The specifics and logistics of each plan are a little different, and we’re more than happy to translate everything and help you implement mega backdoor Roth contributions.

Do I have access to a mega backdoor Roth?

Not every 401k has a mega backdoor opportunity, but it’s worth checking with your HR department if you don’t already know. You can ask about the mega backdoor Roth…they might look at you funny, but don’t give up! Ask them if your plan allows after-tax 401k contributions. If so, you may be in luck. You’ll just need to check with your plan sponsor to see if and how they facilitate conversions from after-tax to Roth (they will know what this means!). In our experience, the mega backdoor option isn’t super common, but, its common enough that you should check with your HR department or poll your co-workers to see if they’re in on the secret. About 25% of plans have this feature in one form or another. You can also ask us, we love to hunt this stuff down!

Pro tip: It’s possible to front-load your 401(k) by increasing your contribution elections for the first part of 2022 until you reach the limit. Since every plan is a little different, the amount you’ll be able to contribute via the mega backdoor (if you have access) will vary from person to person. Also, if maxing out your contributions leaves your net paycheck a little short of your cash flow needs, don’t be afraid to use your after-tax savings or investments to cover any shortfall. Any draws you take to cover the shortfall will get made up over the balance of the year, and the tax savings will compound over time, putting you well ahead vs. potentially missing out on these contributions if the tax law changes.

In Conclusion

The backdoor Roth and mega backdoor Roth funding opportunity is very attractive if you’ve got the opportunity. While they may not be going away with potential new tax law changes, there is definitely a risk as closing this “loophole” has been in the most recent tax bills. And, while it’s unlikely they’d make the change midyear in 2022, we can’t rule it out. So, we recommend maxing these opportunities out early in 2022. Let’s get those backdoor Roth contributions out of the way early!

As always, we love this stuff, if you have questions, please don’t hesitate to reach out!

0 Comments